Welcome: Shenzhen Huayuan Display Control Technique Co.,Ltd.

The SID Business Conference took place during Display Week in May 2025 and covered all the key market segments for displays. Ross Young, VP of Counterpoint Research (Ross has announced his retirement recently), gave an in-depth presentation about the market and technology trends in TV, smartphone, automotive, and IT displays with forecasts for the future. Presentations from display industry executives and Counterpoint Research’s analysts at the Business Conference also gave detailed information about current and future trends.

According to Ross’s keynote presentation:

Display Revenues Rebounded in 2024 – Up 11%

Display Revenues by Technology:

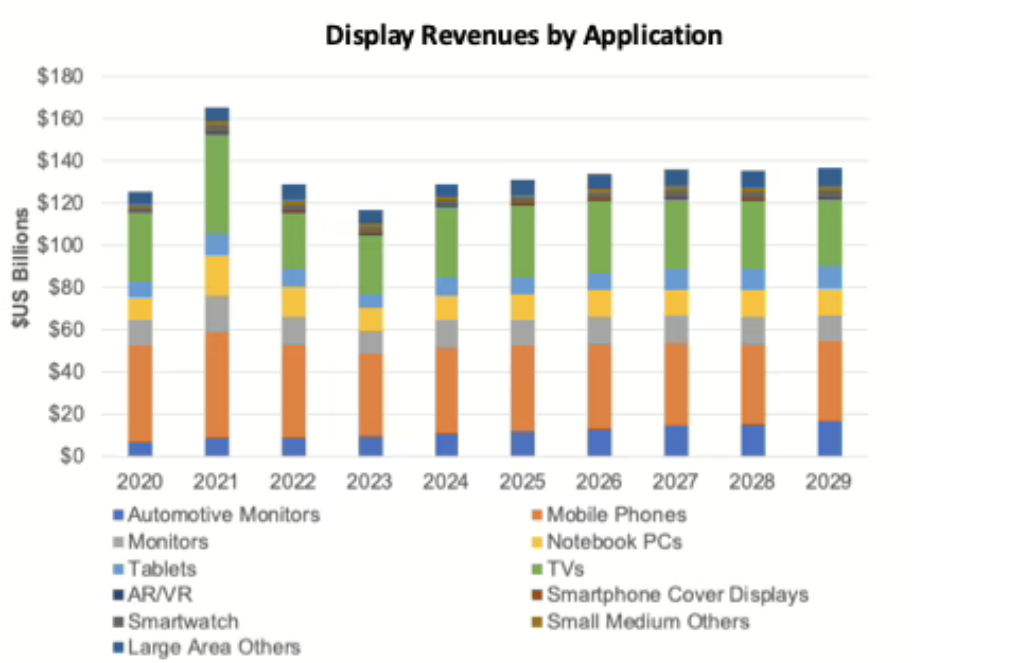

Display Revenues by Application:

Display revenue shares by application (Source: Counterpoint Research)

Richard Kim, SVP of BOE Tech, said in his keynote presentation, “Empowering IoT with display drives premium growth, and 68% of IoT devices have displays.” BOE, the leading LCD supplier, is continuing to develop high-end LCD technology (ADS Pro) solutions and using AI+ for image quality refinement of the display. Eric Cheng, CEO of Tianma America, in his keynote presentation discussed how generative AI is driving changes across the industry, especially in automotive. ChatGPT and DeepSeek are already being used in many cars.

Indrajit Lahiri, Corporate VP of Applied Materials, presented in his keynote, “OLED is primarily adopted in smartphones which have small screens and high ASPs. Breakthrough in OLED scaling is needed to bring OLED to additional markets.” He pointed out that FMM has challenges for small PDL (pixel definition layer) which is needed for higher aperture ratio, and lithography process can deliver it. Applied Materials has introduced MAX OLED solution, a maskless patterning solution using lithography which can enable higher aperture ratio resulting in more than 30% power saving, cost reductions, and design flexibility. It can enable faster time to market as FMM lead time is in months vs. photomask lead time in weeks.

OLED has been gaining only modest unit shares in the IT applications. Cost has been a big challenge. OLED suppliers are planning to shift from Gen 6 to higher Gen 8.7 fabs to lower costs.

As Ross pointed out in his presentation:

Suppliers are now considering photo lithography patterning technology. It has the potential to be used for all applications from MicroOLED to large TV; it could also scale up to Gen10.5 fab. New manufacturing processes will take time to scale and improve yields to reduce costs.

The evolving US tariff situation is impacting smartphone market outlook. Gerrit Schneemann, Senior Analyst at Counterpoint Research, said that “Global smartphone shipment outlook for 2025 was lowered from 4% growth to 1% decline. The primary driver for this decline is the anticipated lower volume in the US.” The situation has reignited efforts to diversify manufacturing away from China. As per Ross Young’s presentation, Smartphone Display Shipments trends:

Name: lily

Mobile:185 7332 9919

Tel:185 7332 9919

Whatsapp:8618573329919

Email:sales@huayuan-lcd.com

Add:Factory No.9, Zhongnan High-tech Intelligent Manufacturing Industrial Park, Tianyuan District, Zhuzhou,Hunan, China, 412000